Questions You Shouldn't Have To Ask Your Financial Advisor

Questions You Shouldn't Have To Ask Your Financial Advisor

by T. Claire Kest, CFP®, CAP®

A financial advisor from Champaign, Illinois, recently submitted a piece entitled "Questions to Ask Your Financial Advisor" in the June 2025 issue of PrimeLife Times. These questions highlight a different approach to financial reviews compared to the proactive style we use at the Hurlow Wealth Management Group.

Here are the questions suggested in the PrimeLife Times article:

- Are my goals still realistic?

- Am I taking on too much--or too little--risk?

- How will life changes affect my investment strategy?

- How are external forces affecting my investment portfolio?

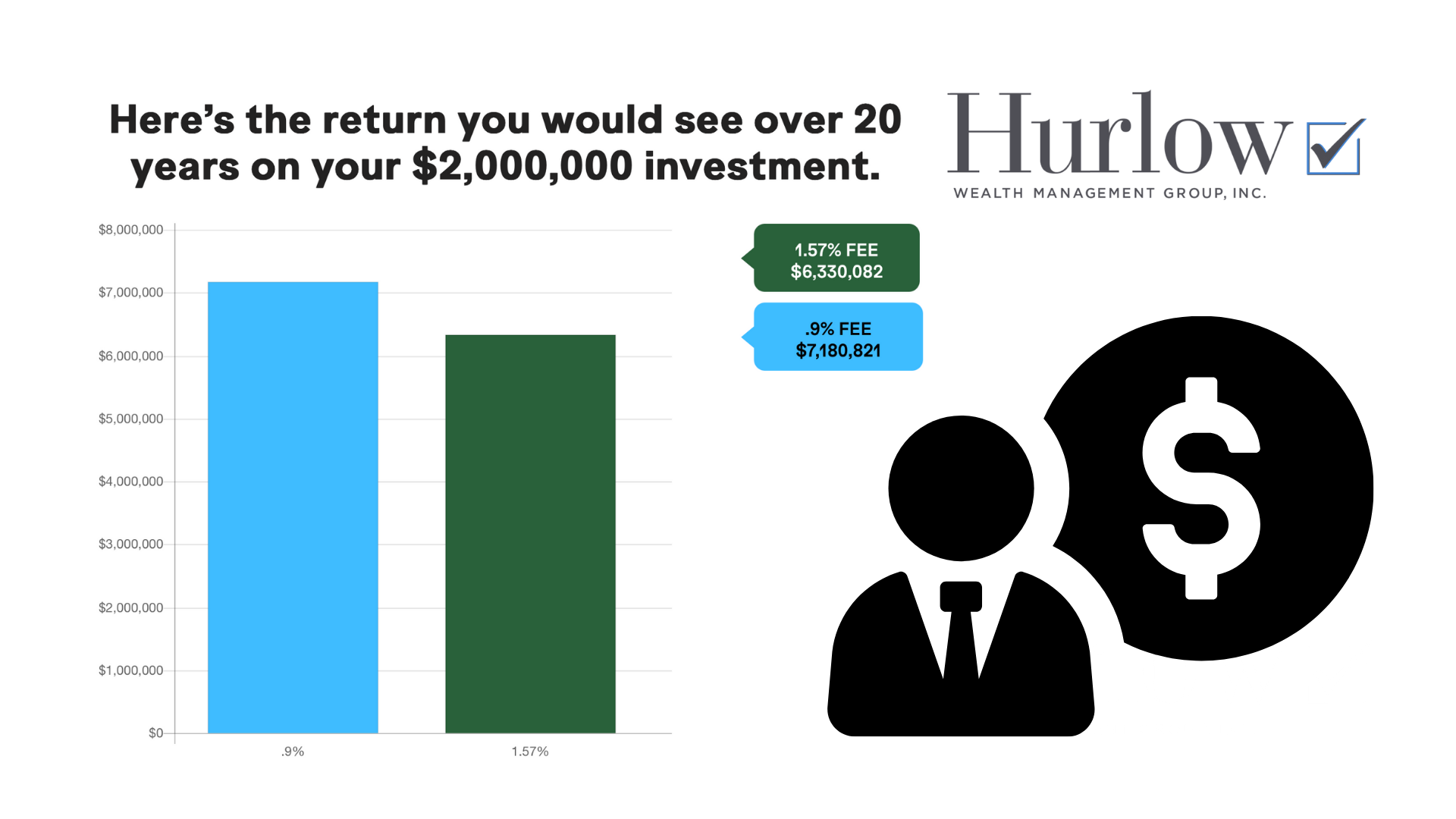

When firms charge 1.35% for investment management, clients should expect their advisor to address these core issues proactively. At Hurlow Wealth Management Group, where our fees are capped at a maximum of 1%, we believe it is our fiduciary duty to anticipate questions and create a level of clarity that leads to peace of mind.

An annual financial review should cover goals, risk, and investment strategy. However, many firms fail to provide this level of service. We often rescue clients who felt uninformed or confused year after year by their former advisors regarding the overall direction of their financial plans.

In our annual comprehensive review, we never expect clients to bring us questions, but we are happy to answer if they do. It is our responsibility as professionals to take the proactive step of informing clients about their financial situation. Here is what clients might expect if they were to have a review with an advisory team at Hurlow Wealth Management Group.

- Start with updates: We want to know if clients have any new additions to their family, changes in their circumstances, or have updated their professional contacts (attorneys, accountants, or insurance agents). While some firms rely on clients to initiate questions about life changes, we take a proactive approach to identifying both challenges and opportunities that arise when life changes. For instance, if they change jobs, we can model how income and retirement plan contributions will affect their goals. Additionally, we can assist them with rollover options for retirement accounts.

- Review Goals: If you're unsure whether your goals are realistic, that may signal your advisor isn't providing ongoing, proactive planning. A fiduciary advisor should clearly communicate the feasibility and appropriateness of goals upfront and review them at least annually as the client's situation changes. Whenever you’re paying advisory fees, it’s worth evaluating the value you receive compared to the level of service and support.

- Review What You Can Control: Some advisors encourage questions about external factors. Our philosophy is different: we focus on strategies within a client’s control because we can’t control external factors like the stock market, tax rates, interest rates or inflation. What we can do, however, is help clients gain a clear understanding of their cash flow, implement tax-mitigation strategies, time distributions effectively, and prepare in advance for potential downturns in the stock market.

- Review Investment Performance and Risk: Understanding risk involves more than just exposure to the stock market. While some advisors put the responsibility on their clients to ask about the level of risk, and make requests to adjust, a fiduciary financial advisor takes on the responsibility of making sure you are invested appropriately. We measure risk in three key ways, how much stock exposure can you take, how much do you need to take and how much are you willing to take. But stock exposure is only one area of risk management. A comprehensive financial plan will also include a review of insurance (life, health, disability, long-term care, auto & home). If your financial advisor does not include a review of the other areas of risk exposure, how can they answer the question, "Am I taking on too much--or too little--risk?"

If you are currently working with an advisor and do not have answers to these questions, it may be time to consider interviewing a new advisor. Here are some questions that the Securities and Exchange Commission recommends asking when you interview a new advisor:

- Are you registered with our state securities regulator?

- Do you have legal or disciplinary history?

- How long has your firm been in business?

- What training and experience do you have?

- What is your investment philosophy?

- Describe your typical client

- How do you get paid?

- Do you make more if I buy this stock (or bond, or mutual fund) rather than another?

True fiduciary relationships shouldn't leave you wondering about the fundamentals of your financial health. At Hurlow Wealth Management Group, it's our responsibility to proactively review your complete financial plan to make sure you're on the right track. For over two decades, our financial advisors have helped Midwest Millionaires find clarity, make decisions with confidence, and feel comfort in retirement. If you would like a complimentary consultation to experience the fiduciary difference, CLICK HERE to schedule an introductory call today.